Filter out the noise and focus on the important trends.

By Aaron Brown

3 January 2018

Riding the wave. Photographer: Jung Yeon-Je/AFP/Getty Images

Bitcoin rose 88 percent from Dec. 1 to 19, then fell 23 percent by Dec. 30, a net 44 percent increase for the month. Attention naturally focused on those events, but the important longer-term story is what's happening within the entire cryptocurrency sector.

The market value of all non-bitcoin crypto assets rose 153 percent during bitcoin's upswing, and 4 percent more while bitcoin declined, for a return of 162 percent for December to a diversified investor in crypto ex-bitcoin. But there are more than 3,000 cryptocurrencies, tokens and assets. Each can have communities, networks and tokens that overlap but are not identical. And each has different technical underpinnings and use cases, and none has traditional financial metrics. So, how can an investor make sense of the market?

A mathematical tool called factor analysis can filter out noise. Instead of studying technical indicators like hashing power, block size and supply control, it can identify the user experience factors that seem to be important for prices. We use statistics to extract the main factors that seemed to drive most of the moves of cryptoassets relative to one another in December, ignoring prices in dollars.

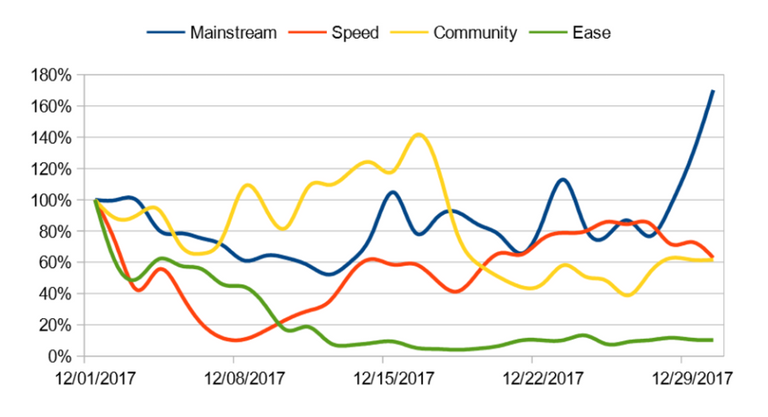

The chart above shows the four factors that seem to explain most of the December price movements. Each factor is a portfolio with long and short positions in many cryptocurrencies, which are determined solely by statistics. I looked at the factors and choose the names above.

For example, the Mainstream factor has positive weights on Ripple, Cardano and Stellar, currencies that are designed to get along with regulations and institutions. It places negative weights on the likes of Dash, Monero and Zcash, which are designed for user privacy.

The Mainstream factor drifted down for the first couple of weeks, recovered in subsequent weeks, then shot up at the end. My guess is it declined due to the expectation that bitcoin would go mainstream with Cboe and CME futures trading, plus an ETF in the near future. If regulators and institutions accept bitcoin, there is less need for regulation-friendly currencies, while some current bitcoin users could switch to more private coins. The factor likely drifted back up as futures trading did not lead to large bitcoin holders transferring exposure to financial institutions. The spike at the end suggests a possibly transitory optimism that bitcoin will remain a currency for technophiles and libertarians, clearing the way for inoffensive alternatives.

The second and fourth factors, Speed and Ease, relate to transaction convenience. Speed favors currencies such as Litecoin, Ripple, Monero and Ethereum, with negative weight on bitcoin. Ease has positive weights on currencies such as Litecoin and Dash, which are cheap to use and relatively user-friendly. These factors drifted down in the first couple of weeks, likely for the same reason: If bitcoin was ready for prime time, then Speed and Ease would not be enough to compete.

When bitcoin had a disappointing debut, Speed mostly recovered but Ease stayed down. As there was little technical news on either subject for the month, I suspect the feedback from people who looked at cryptocurrencies for the first time led to the conclusion that Speed was a major competitive advantage, but ease of use was not. One of the most important things in crypto at the moment is a massive increase in the breadth of user feedback, we are learning which cryptocurrencies will be favored outside the small group of technophile early adopters.

The third factor, Community, refers to the size, quality and enthusiasm of the developer and support community. A cryptocurrency is not just an idea, it needs lots of code -- which has to be maintained -- and extensive hardware in one form or another. It needs a broad base of sophisticated users to try new features and provide feedback. It needs committed, long-term capital and a broad base of holders. Bitcoin and Ethereum have the largest weights on this factor; Ripple, Monero and Zcash have smaller positive weights. There are negative weights on currencies that have little or no active development, or less-than-sterling reputations, or have had hacks or scandals or disputes in their past.

Community outperformed and then crashed. 3 My guess is that faith in established cryptocurrency communities was shaken by the sudden dollar flood; kind of like a rock band falling apart after having a hit. Some people fought the intrusion of Wall Street, others took the money and ran. Some felt cheated by how little they had to show for years of work on a group project, when others who had contributed far less were multimillionaires. When visionary idealists collide with big money, the results are hard to predict.

None of this is investment advice. Some people will look at the chart above and load up on Mainstream currencies while shorting privacy ones, hoping the trend is their friend. Others will note that you can buy Ease very cheaply. Factors can help you filter out the noise to focus on the important trends, but they can't tell you what those trends will do in 2018.

Bloomberg Prophets

Professionals offering actionable insights on markets, the economy and monetary policy. Contributors may have a stake in the areas they write about.

To be clear, statistics cannot tell us the name of a factor, something like “value” or “growth.” What it can do is construct portfolios with net zero cost that explain as much as possible about all the individual moves. Because the portfolios have equal long and short positions, the movements of cryptocurrencies in general in dollar terms are irrelevant. The factors give us insight into what is driving cryptocurrency prices versus one another.

Bitcoin and its clones get smaller negative weights and Ethereum is near zero and its competitors have small positive weights.

A few days later, bitcoin crashed.

credits: bloomberg

upvoted done your post 52%[email protected]